Asset Location

01/20/2024Blog Categories

You’re probably already familiar with the three most important factors in real estate:

Location. Location. Location.

Asset location is a similarly important, if less familiar best practice for keeping as much of your wealth as possible – after taxes have taken their toll. Given how steep that toll can be, it’s worth knowing more about how to benefit from proper asset location.

Each of these accounts is taxed differently and may have various investment time frames. Asset location refers to which types of investments reside in which types of these accounts.

It makes intuitive sense to locate bonds, REITS, and other asset classes according to their expected tax efficiencies. But it’s not as easily implemented as you might think.

First, there is only so much room in your tax-sheltered accounts. After all, if there were unlimited opportunities to avoid paying income taxes on your investments, you’d simply shelter all of them and be done with it. In reality, challenging trade-offs must be made to ensure you’re making the best use of your tax-sheltered “space.”

Second, it’s not just about tax-sheltering your assets. Eventually, you’ll also want to spend or bequeath them, so you want to plan for that too. Here are some ideas on how to do that.

While you may not even know if you are missing out on optimal asset location, the resulting wealth unnecessarily lost to taxes can be very real. Here are some reasons your asset location planning may fall short:

It’s an art and a science to apply effective asset location to your unique, often complex wealth management. That said, the efforts can pay for themselves many times over by minimizing taxes for you and your heirs.

Can we answer additional questions about this often-overlooked aspect of investing? Feel free to reach out.

Brandon

Location. Location. Location.

Asset location is a similarly important, if less familiar best practice for keeping as much of your wealth as possible – after taxes have taken their toll. Given how steep that toll can be, it’s worth knowing more about how to benefit from proper asset location.

Asset Location: A Working Definition

Let’s begin by noting that asset location should not be confused with asset allocation. The two are related, but different portfolio management techniques.- Asset allocation is dividing your money among different asset class holdings – such as 50% stocks, 50% bonds. The purpose is to create an appropriate balance between seeking higher market returns while managing the risks involved.

- Asset location(today’s focus) is deciding where to hold your various assets among your taxable and tax-sheltered accounts. The purpose is to invest as tax-efficiently as possible.

The 3 Main Types of Investment Accounts

As investors, we have several different types of accounts that can be aligned with specific investing goals. Here’s the summary of each category and how they work:- Taxable accounts such as traditional brokerage accounts hold securities (stocks, bonds, mutual funds, ETFs) that are taxed when you earn dividends or interest, or you realize capital gains by selling investments that went up in value.

- Tax-deferred accounts like traditional 401(k)s, 403(b)s, annuities, and IRAs allow payment of taxes to be delayed until the money is withdrawn, when all or a portion of it is taxed as ordinary income.

- Tax-exempt accounts like Roth IRAs, Roth 401(k)s, and Roth 403(b)s, require contributions to be made with after-tax dollars and do not provide a tax deduction up front, but they allow the investor to avoid further taxation (as long as the rules are followed). Health savings accounts (HSAs) are included here also. They allow you to make pretax contributions, and their growth and withdrawals are not taxed federally if used for qualified health expenses.

Each of these accounts is taxed differently and may have various investment time frames. Asset location refers to which types of investments reside in which types of these accounts.

How It Happens

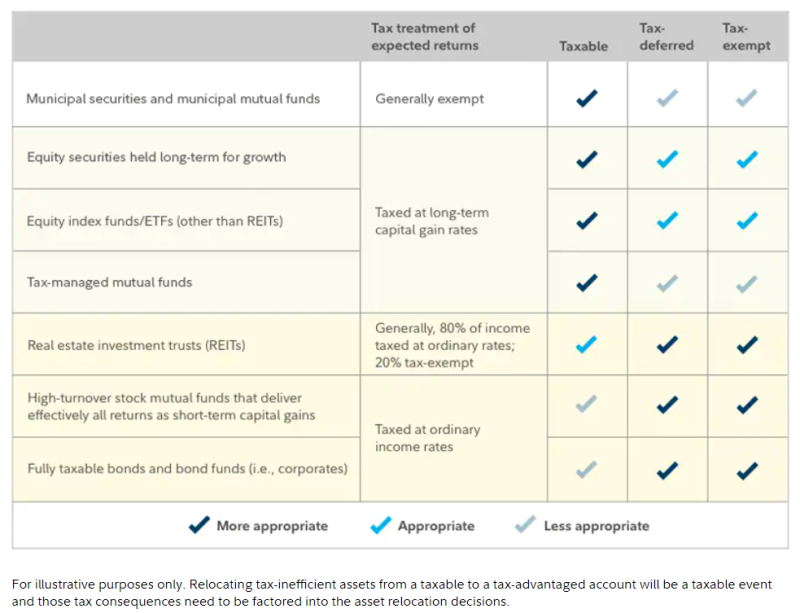

By locating your least tax-efficient investments in your tax-sheltered accounts (#2 and #3 above), you can minimize or even eliminate tax inefficiencies. For example, typically (but not always!) holdings such as fixed income and REIT funds are less tax-efficient than stocks. And among stock asset classes, some are more or less tax-efficient than others. Here’s a chart that generally works for solid guidance:

It makes intuitive sense to locate bonds, REITS, and other asset classes according to their expected tax efficiencies. But it’s not as easily implemented as you might think.

First, there is only so much room in your tax-sheltered accounts. After all, if there were unlimited opportunities to avoid paying income taxes on your investments, you’d simply shelter all of them and be done with it. In reality, challenging trade-offs must be made to ensure you’re making the best use of your tax-sheltered “space.”

Second, it’s not just about tax-sheltering your assets. Eventually, you’ll also want to spend or bequeath them, so you want to plan for that too. Here are some ideas on how to do that.

- Managing your bigger picture – Before deciding where to locate your assets, first determine your proper asset allocation based on your unique goals and risk tolerances. Only then is it appropriate to determine where those holdings should reside for tax efficiency.

- Planning for your goals and timeframe – Is retirement near or far? Do you want to leave a legacy? Will you be withdrawing from a Traditional IRA many years before your Roth IRA? These spending, estate planning, and other needs may override, or at least influence your optimal asset location.

- Managing tax-sheltered accounts – What are your tax-sheltered account opportunities among Roth IRAs, traditional IRAs, and company retirement plans? How much room do you have in each, and which specific holdings in which exact accounts are expected to give you the most tax-efficient outcomes? How might evolving tax codes impact your plans?

- Considering other tax-planning needs – We also consider the benefits of holding assets in taxable accounts, such as being able to use foreign tax credits from international investments, harvest capital losses against capital gains, allow your heirs to receive a step-up in basis upon inheritance, and/or donate highly appreciated shares to charity to reduce capital gains taxes.

The Art and Science of Asset Location

While you may not even know if you are missing out on optimal asset location, the resulting wealth unnecessarily lost to taxes can be very real. Here are some reasons your asset location planning may fall short:- Missing pieces – Through the years, families usually accumulate a jumble of individual and retirement plan accounts and financial service providers. As your assets grow, it becomes an increasing challenge to organize them into a cohesive whole.

- Missing expertise – Even if you have a handle on all your holdings, effective asset location should be considered within the multiple, often competing components of your total wealth. This calls for multidisciplinary oversight across investment management, tax planning, and estate planning alike.

- Missing oversight – Asset location is not a set-and-forget activity. As your own goals, the market, and government regulations evolve, your assets require ongoing management to retain their desired efficiencies.

It’s an art and a science to apply effective asset location to your unique, often complex wealth management. That said, the efforts can pay for themselves many times over by minimizing taxes for you and your heirs.

Can we answer additional questions about this often-overlooked aspect of investing? Feel free to reach out.

Brandon