Q1 – 2025: Brandon’s Quarterly Market Commentary

04/07/2025Blog Categories

The first quarter of 2025 certainly was a doozy!

What we saw – after two years of relatively smooth sailing and positive market returns – was a rude awakening. The national conversation changed from our economy navigating a “soft landing” to wondering what effect tariffs would have on the world. US stocks hit new records in February, but quickly declined just a few weeks into March.

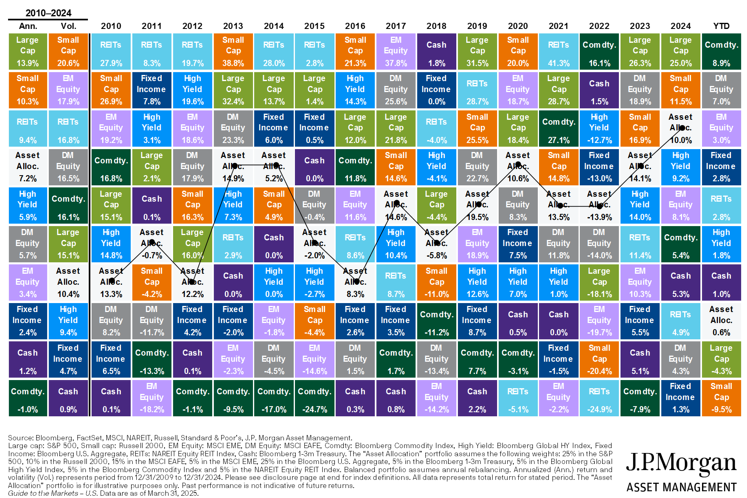

As we reflect on the past 90 days, I’d encourage people to see through the gloomy headlines. Things might not have been as bad as it would appear. And for investors who have been patient holding diversified portfolios, they’ll likely find their accounts held up pretty well. Here’s how the returns looked in general (YTD is through 3-31-2025):

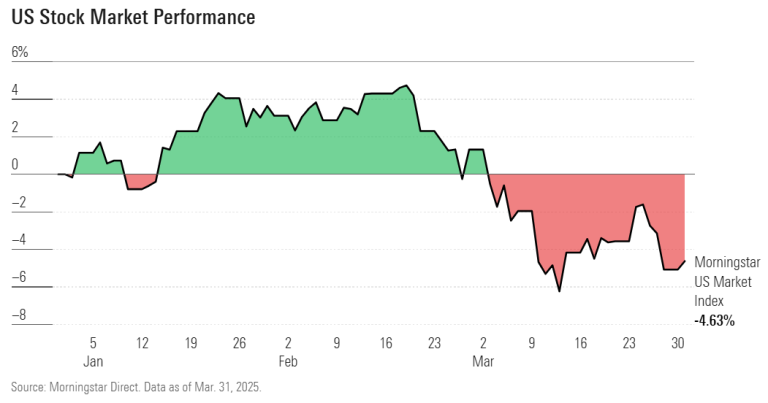

Even though the S&P 500 had its worst quarter since the second quarter of 2022, it wasn’t all doom and gloom. Seven of the 11 sectors were positive. Safe havens of outperformance were observed with value and dividend stocks. The energy and healthcare sectors outperformed others. In addition, non-US stocks rallied, and bonds did well. Lastly, gold was a big winner.

Nonetheless, here’s a visual of US stock reversal from Q1:

So what got hammered if I just pointed out the good performers? Well, we saw a reversal of some of last year’s top performers—namely, large growth companies and technology specifically. The “Magnificient 7”, which got all the praise in 2024, were down a collective 18% (ranging from -1 % to -35 % individually).

For those following the crypto scene – bitcoin and others were hit pretty hard. Small cap companies also struggled more than large caps.

Here’s how the U.S. style box looked for the quarter:

As the US stock market lost ground, the international markets surged. We saw strong performance from companies in China, Germany, and the Eurozone markets. Investors diversifying their equity exposure internationally were rewarded in Q1.

For bond investors, performance was strong here as well. Those with various pieces of the bond market saw low single-digit returns for the quarter.

Yields on the 10-year Treasury note dropped from 4.54% at the beginning of the quarter to 4.23% at the end of the quarter. CD shoppers hoping to renew their certificates of deposit were faced with more of a dilemma due to the corresponding drop in CD rates.

Another observation I’ll make is the notable increase in stock market volatility. Investors grappled with the increased uncertainty of the tariff policy and evolving outlook. We often look at the “VIX” (aka volatility index) to gauge market sentiment. After seeing a VIX range between 13 and 18 for the bulk of the 2024, by month-end March 2025 it was around a 24 level. This indicates that the next 30 days in the markets could increase uncertainty.

Looking Ahead:

I believe that the recent market volatility we’ve seen of late will persist, at least in the short term. Until we see how global trade is impacted and learn which tariffs get adjusted or not, we may see the market worry. I am a big believer in having investors remain calm and have a plan to reposition or rebalance. For example, look for opportunities to remain invested but consider swapping out something showing a loss for a similar (but not too similar) investment.

Since tariffs are mentioned in the news everywhere we look, let me address that briefly. Tariffs are essentially taxes on imported goods. They aim to encourage domestic manufacturing and help manage the trade deficit. While well-intended, tariffs can also mean higher costs for companies importing materials or goods from abroad. Trade wars may be an unintended outcome.

The real impact? Some industries, like manufacturing, may face higher costs, which could impact profits. Other sectors, like healthcare and utilities, may be less affected due to their primarily domestic operations.

On some levels, the extreme nature of the proposed measures (some calling them absurd) could indicate that these may be short-lived. Could this be a negotiating tactic by the White House? Maybe. It would appear that this methodology reflects an effort to impose leverage, but only time will tell. It’s feasible that the tariffs could be more tactical in nature, rather than permanent.

Final thoughts:

You might ask, “What does this all mean to me?” I’ll say this: Short-term volatility is normal in financial markets. Does it feel great in periods of volatility? Most would say NO!

The S&P 500 has gained about 10.5% annually since its inception in 1957. This covers almost a 70-year period of wars, recessions, political upheavals, “irrational exuberance,” and boom/bust cycles. Investors who maintained discipline and remained in the market over the long term have been rewarded.

And despite the uncertainties that may take weeks or months to get through, consider that we still have strong corporate earnings and a resilient U.S. consumer base. Valuations to some stock sectors are either fairly valued or even undervalued. Yes there have been signs of the economy softening, and the short-term path is unclear. Still, there are opportunities to look for.

My priority is helping you remain confident in your long-term investment strategy. Reach out directly if you want to chat further.

Brandon

What we saw – after two years of relatively smooth sailing and positive market returns – was a rude awakening. The national conversation changed from our economy navigating a “soft landing” to wondering what effect tariffs would have on the world. US stocks hit new records in February, but quickly declined just a few weeks into March.

As we reflect on the past 90 days, I’d encourage people to see through the gloomy headlines. Things might not have been as bad as it would appear. And for investors who have been patient holding diversified portfolios, they’ll likely find their accounts held up pretty well. Here’s how the returns looked in general (YTD is through 3-31-2025):

Looking back, here are some observations.

Even though the S&P 500 had its worst quarter since the second quarter of 2022, it wasn’t all doom and gloom. Seven of the 11 sectors were positive. Safe havens of outperformance were observed with value and dividend stocks. The energy and healthcare sectors outperformed others. In addition, non-US stocks rallied, and bonds did well. Lastly, gold was a big winner.Nonetheless, here’s a visual of US stock reversal from Q1:

So what got hammered if I just pointed out the good performers? Well, we saw a reversal of some of last year’s top performers—namely, large growth companies and technology specifically. The “Magnificient 7”, which got all the praise in 2024, were down a collective 18% (ranging from -1 % to -35 % individually).

For those following the crypto scene – bitcoin and others were hit pretty hard. Small cap companies also struggled more than large caps.

Here’s how the U.S. style box looked for the quarter:

As the US stock market lost ground, the international markets surged. We saw strong performance from companies in China, Germany, and the Eurozone markets. Investors diversifying their equity exposure internationally were rewarded in Q1.

For bond investors, performance was strong here as well. Those with various pieces of the bond market saw low single-digit returns for the quarter.

Yields on the 10-year Treasury note dropped from 4.54% at the beginning of the quarter to 4.23% at the end of the quarter. CD shoppers hoping to renew their certificates of deposit were faced with more of a dilemma due to the corresponding drop in CD rates.

Another observation I’ll make is the notable increase in stock market volatility. Investors grappled with the increased uncertainty of the tariff policy and evolving outlook. We often look at the “VIX” (aka volatility index) to gauge market sentiment. After seeing a VIX range between 13 and 18 for the bulk of the 2024, by month-end March 2025 it was around a 24 level. This indicates that the next 30 days in the markets could increase uncertainty.

Looking Ahead:

I believe that the recent market volatility we’ve seen of late will persist, at least in the short term. Until we see how global trade is impacted and learn which tariffs get adjusted or not, we may see the market worry. I am a big believer in having investors remain calm and have a plan to reposition or rebalance. For example, look for opportunities to remain invested but consider swapping out something showing a loss for a similar (but not too similar) investment.Since tariffs are mentioned in the news everywhere we look, let me address that briefly. Tariffs are essentially taxes on imported goods. They aim to encourage domestic manufacturing and help manage the trade deficit. While well-intended, tariffs can also mean higher costs for companies importing materials or goods from abroad. Trade wars may be an unintended outcome.

The real impact? Some industries, like manufacturing, may face higher costs, which could impact profits. Other sectors, like healthcare and utilities, may be less affected due to their primarily domestic operations.

On some levels, the extreme nature of the proposed measures (some calling them absurd) could indicate that these may be short-lived. Could this be a negotiating tactic by the White House? Maybe. It would appear that this methodology reflects an effort to impose leverage, but only time will tell. It’s feasible that the tariffs could be more tactical in nature, rather than permanent.

Final thoughts:

You might ask, “What does this all mean to me?” I’ll say this: Short-term volatility is normal in financial markets. Does it feel great in periods of volatility? Most would say NO!The S&P 500 has gained about 10.5% annually since its inception in 1957. This covers almost a 70-year period of wars, recessions, political upheavals, “irrational exuberance,” and boom/bust cycles. Investors who maintained discipline and remained in the market over the long term have been rewarded.

And despite the uncertainties that may take weeks or months to get through, consider that we still have strong corporate earnings and a resilient U.S. consumer base. Valuations to some stock sectors are either fairly valued or even undervalued. Yes there have been signs of the economy softening, and the short-term path is unclear. Still, there are opportunities to look for.

My priority is helping you remain confident in your long-term investment strategy. Reach out directly if you want to chat further.

Brandon