Q2 – 2025: Brandon’s Quarterly Market Commentary

07/06/2025Blog Categories

What a turnaround in Q2!

Just three months ago, the markets were slumping due to the Trump administration’s tariff announcements. The negative sentiment continued into early April, but suddenly things changed. Almost all stocks jumped higher once more tariffs were either paused or reduced!

US stocks ended the month of June by hitting new records, just as they had earlier in February. And their quick rebound was dizzying. What might have been more impressive is the trend of international stocks continuing to outperform the US markets. More on that below.

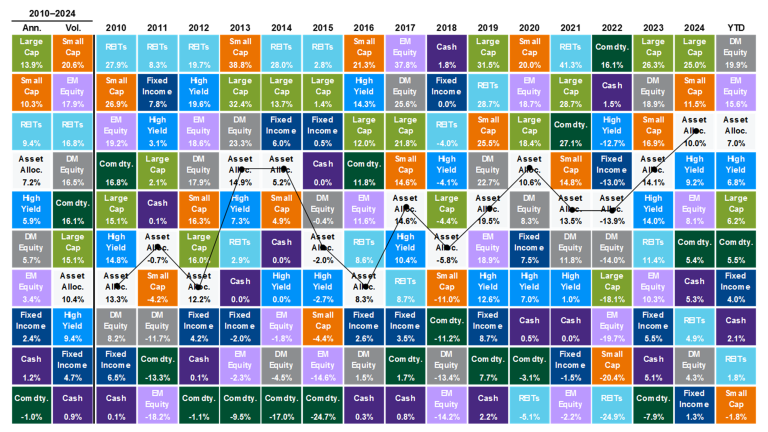

As we take a breather and reflect, let’s see how the various asset classes look so far this year compared to prior years (YTD through 6-30-2025):

Source: Bloomberg, FactSet, MSCI, NAREIT, Russell, Standard & Poor’s, J.P. Morgan Asset Management. Large Cap: S&P 500, Small Cap: Russell 2000, EM Equity: MSCI EME, DM Equity: MSCI EAFE, Comdty: Bloomberg Commodity Index, High Yield: Bloomberg Global HY Index, Fixed Income: Bloomberg U.S. Aggregate, REITs: NAREIT Equity REIT Index, Cash: Bloomberg 1-3m Treasury. The “Asset Allocation” portfolio is for illustrative purposes only and assumes annual rebalancing with the following weights: 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Bloomberg U.S. Aggregate, 5% in the Bloomberg 1-3m Treasury, 5% in the Bloomberg Global High Yield Index, 5% in the Bloomberg Commodity Index, and 5% in the NAREIT Equity REIT Index. Annualized (Ann.) return and volatility (Vol.) represents the period from 12/31/2009 to 12/31/2024. Please see the disclosure page at the end for index definitions. All data represent total return for stated period. Past performance is not indicative of future returns.

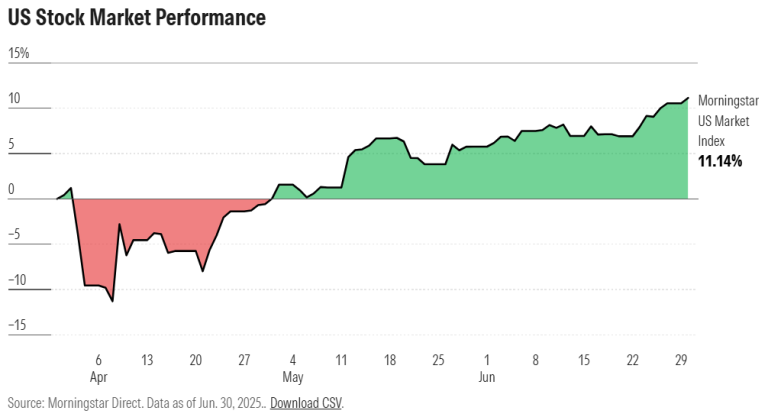

Here’s a visual of the US stock reversal from Q2, which is almost an inverted flip from Q1:

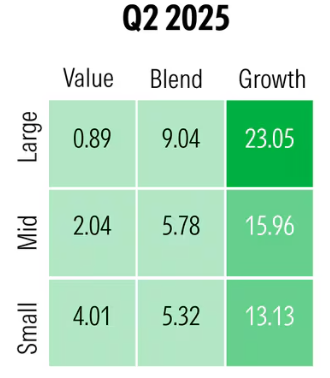

Here’s how the U.S. style box looked for the quarter. Notably, while everything here in the US was in the green, growth stocks outperformed value stocks. Similarly, large-cap stocks outperformed small-cap stocks:

Interestingly enough, international markets proceeded full steam ahead and relatively outperformed US markets. Europe, Canada, and Japanese stocks all outpaced the US. Emerging markets (except for China) were solid as well. Investors diversifying their equity exposure internationally have been rewarded nicely thus far in 2025.

The bond market was also mainly in the green, albeit with a more muted performance than its strong showing in Q1. The diversified index of various US bonds (aka the Bloomberg Agg Index) is up ~3.7% so far this year.

Yields on the 10-year Treasury note were flat (4.23%) for the quarter, but they did fluctuate as high as 4.6% in May. The Fed kept rates unchanged in June but continues to walk a tightrope between inflation and economic growth.

Commodities had a solid quarter, as gold continued to climb, as did the mining companies. Oil prices fell overall but traded in a pretty wide and volatile range due to geopolitical tensions.

As we reflect on the past quarter, I encourage investors to take it with a grain of salt. My last quarterly commentary indicated that things might not have been as bad as they appeared. In this commentary, I emphasize that while things look promising on your mid-2025 statements, let’s not get ahead of ourselves. Things can quickly change, for better or worse, in either direction.

Additional Discussion Points:

If you have been following me for some time, you know I believe in diversification. The way international stocks have been outperforming lately only reinforces that point.

The Trump Administration’s tariffs are part of a broader trend toward deglobalization. (Think Brexit, Russia’s invasion of Ukraine, Covid-era supply chain problems and the first Trump Administration’s tariffs, to name a few deglobalization developments.) This trend is evident in global trade numbers: Foreign direct investment climbed between 1970 and 2007, and has fallen dramatically since.

In the U.S., a retreat from global trade could drag on economic growth and push inflation higher, creating headwinds for stock and bond investors. But deglobalization has a silver lining for the well-diversified investor. The less connected global economies are, the less their markets are likely to move in sync with each other. The upshot: International stocks and bonds may provide more diversification away from U.S. assets than they have in recent decades.

That would be a welcome development. Correlations between U.S. and international stocks jumped from 0.54 in the 1990s to 0.87 between 2000 and 2022, meaning international equity allocations didn’t provide as much diversification as they once had. (The lower the correlation between two investments, the better they diversify each other.)

The rise in correlations might be reversing. U.S. and international stocks behaved very differently during the first half of the year. In the first half of the year, the S&P 500 rose 5.7%, while the MSCI EAFE gained 17.3%.

I feel pretty confident by saying that diversifying globally is not optional, rather it is a strategic imperative! When you spread out your bets by diversifying across asset classes, geographies, sectors, and industries, you reduce the risks associated with any particular outcome. In this case, diversifying internationally might help buoy a portfolio if U.S. stocks are hit by slower growth and higher inflation.

Final thoughts:

As the third quarter unfolds, I don’t think I’m going out on a limb by saying we’ll see continued complexity. We’ve got ongoing discussions about the national debt, geopolitical situations, the impact of tariffs, and, most recently, the effect of the “One Big Beautiful Act.” We’ll be tracking these developments and will stay nimble and adaptable.

I don’t think we should be lulled into complacency or stunned by any upcoming twists and turns. It’s all part of investing. We’ll continue to look for opportunities and inefficiencies and make the best decisions with all relevant information. Please reach out if you want to discuss further.

Brandon

Just three months ago, the markets were slumping due to the Trump administration’s tariff announcements. The negative sentiment continued into early April, but suddenly things changed. Almost all stocks jumped higher once more tariffs were either paused or reduced!

US stocks ended the month of June by hitting new records, just as they had earlier in February. And their quick rebound was dizzying. What might have been more impressive is the trend of international stocks continuing to outperform the US markets. More on that below.

As we take a breather and reflect, let’s see how the various asset classes look so far this year compared to prior years (YTD through 6-30-2025):

Source: Bloomberg, FactSet, MSCI, NAREIT, Russell, Standard & Poor’s, J.P. Morgan Asset Management. Large Cap: S&P 500, Small Cap: Russell 2000, EM Equity: MSCI EME, DM Equity: MSCI EAFE, Comdty: Bloomberg Commodity Index, High Yield: Bloomberg Global HY Index, Fixed Income: Bloomberg U.S. Aggregate, REITs: NAREIT Equity REIT Index, Cash: Bloomberg 1-3m Treasury. The “Asset Allocation” portfolio is for illustrative purposes only and assumes annual rebalancing with the following weights: 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Bloomberg U.S. Aggregate, 5% in the Bloomberg 1-3m Treasury, 5% in the Bloomberg Global High Yield Index, 5% in the Bloomberg Commodity Index, and 5% in the NAREIT Equity REIT Index. Annualized (Ann.) return and volatility (Vol.) represents the period from 12/31/2009 to 12/31/2024. Please see the disclosure page at the end for index definitions. All data represent total return for stated period. Past performance is not indicative of future returns.

Looking back, here are some observations:

The S&P 500 followed a weak first quarter with one of the better quarters seen in recent years. Eight of the 11 sectors were positive, led by strong rebounds in communications and technology names. Laggards included energy and healthcare stocks.Here’s a visual of the US stock reversal from Q2, which is almost an inverted flip from Q1:

Here’s how the U.S. style box looked for the quarter. Notably, while everything here in the US was in the green, growth stocks outperformed value stocks. Similarly, large-cap stocks outperformed small-cap stocks:

Interestingly enough, international markets proceeded full steam ahead and relatively outperformed US markets. Europe, Canada, and Japanese stocks all outpaced the US. Emerging markets (except for China) were solid as well. Investors diversifying their equity exposure internationally have been rewarded nicely thus far in 2025.

The bond market was also mainly in the green, albeit with a more muted performance than its strong showing in Q1. The diversified index of various US bonds (aka the Bloomberg Agg Index) is up ~3.7% so far this year.

Yields on the 10-year Treasury note were flat (4.23%) for the quarter, but they did fluctuate as high as 4.6% in May. The Fed kept rates unchanged in June but continues to walk a tightrope between inflation and economic growth.

Commodities had a solid quarter, as gold continued to climb, as did the mining companies. Oil prices fell overall but traded in a pretty wide and volatile range due to geopolitical tensions.

As we reflect on the past quarter, I encourage investors to take it with a grain of salt. My last quarterly commentary indicated that things might not have been as bad as they appeared. In this commentary, I emphasize that while things look promising on your mid-2025 statements, let’s not get ahead of ourselves. Things can quickly change, for better or worse, in either direction.

Additional Discussion Points:

If you have been following me for some time, you know I believe in diversification. The way international stocks have been outperforming lately only reinforces that point. The Trump Administration’s tariffs are part of a broader trend toward deglobalization. (Think Brexit, Russia’s invasion of Ukraine, Covid-era supply chain problems and the first Trump Administration’s tariffs, to name a few deglobalization developments.) This trend is evident in global trade numbers: Foreign direct investment climbed between 1970 and 2007, and has fallen dramatically since.

In the U.S., a retreat from global trade could drag on economic growth and push inflation higher, creating headwinds for stock and bond investors. But deglobalization has a silver lining for the well-diversified investor. The less connected global economies are, the less their markets are likely to move in sync with each other. The upshot: International stocks and bonds may provide more diversification away from U.S. assets than they have in recent decades.

That would be a welcome development. Correlations between U.S. and international stocks jumped from 0.54 in the 1990s to 0.87 between 2000 and 2022, meaning international equity allocations didn’t provide as much diversification as they once had. (The lower the correlation between two investments, the better they diversify each other.)

The rise in correlations might be reversing. U.S. and international stocks behaved very differently during the first half of the year. In the first half of the year, the S&P 500 rose 5.7%, while the MSCI EAFE gained 17.3%.

I feel pretty confident by saying that diversifying globally is not optional, rather it is a strategic imperative! When you spread out your bets by diversifying across asset classes, geographies, sectors, and industries, you reduce the risks associated with any particular outcome. In this case, diversifying internationally might help buoy a portfolio if U.S. stocks are hit by slower growth and higher inflation.

Final thoughts:

As the third quarter unfolds, I don’t think I’m going out on a limb by saying we’ll see continued complexity. We’ve got ongoing discussions about the national debt, geopolitical situations, the impact of tariffs, and, most recently, the effect of the “One Big Beautiful Act.” We’ll be tracking these developments and will stay nimble and adaptable.I don’t think we should be lulled into complacency or stunned by any upcoming twists and turns. It’s all part of investing. We’ll continue to look for opportunities and inefficiencies and make the best decisions with all relevant information. Please reach out if you want to discuss further.

Brandon