Q3 – 2025: Brandon’s Quarterly Market Commentary

10/06/2025Blog Categories

We keep on keepin’ on! Equities continued their recovery that began after the sharp April pullback.

US stocks surged to record highs in Q3. Markets were buoyed by strong AI-related investments, resilient corporate earnings, and expectations of future Fed rate cuts. International markets were strong as well.

While the bullish sentiment and optimism linger heading into Q4, let’s review how the various asset classes look so far this year compared to prior years (YTD through 9-30-2025):

The S&P 500 specifically followed up a strong second quarter with a third quarter that saw the index hit 23 record highs. Ten of the 11 sectors were positive, led by communications and technology names for the second consecutive quarter. The laggards were defensive stocks (the lone negative sector). Healthcare stocks finally turned positive for the year. Also of note, tech stocks now account for more than 50% of the US stock market cap, and defense stocks are at an all-time low (@16%)!

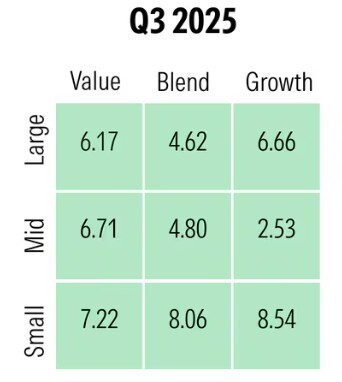

Here’s how the U.S. style box looked for the quarter. Notably, large-cap growth stocks and large-cap value stocks performed similarly but were both outperformed by small-cap stocks:

International markets ticked higher, with emerging markets (China, Canada) outpacing the more developed international markets (Japan, Europe). Investors diversifying their equity exposure internationally continue to be rewarded nicely in 2025 as it outperforms the U.S. by double digits.

Yields on the 10-year Treasury note ended at 4.16% for the quarter, down slightly from July. The drop in yields helped bond investors pick up some price appreciation in their portfolios. Most bond groups were up 2-3% for the previous 3 months.

Gold had another quarter of double-digit gains. Now up 46% YTD (!), the precious metal continues to benefit from geopolitical tensions, a weaker US dollar, and strong inflows from investors seeking a safe haven. The headscratcher, though, is that gold is the usual go-to when traders suspect trouble. We don’t usually see it do so well when the stock market is also doing well.

There were not many negatively performing asset classes in Q3, but oil prices slumped more than 4% in the quarter, as did copper.

Additional Discussion Points:

We just witnessed the Federal Reserve cut interest rates by 1/4 of a percentage point in September. Could we see some more cuts in the near future? Very likely. If the Fed sees proof that the economy is slowing further (due to tariffs, the job market, etc.) they’d be inclined to lower rates further. I am not into predicting rate cuts, but based on what strategists say, most anticipate another rate cut by year-end.

Risks of recession have eased, but remain non-zero. We never know when we are actually IN a recession since, by definition, it’s always determined by what’s happened in the past. But we continue to hear rumblings of that coming to the surface.

What we do measure in real time is volatility. Volatility in the U.S. and international markets declined significantly in the third quarter as the shock of tariff-related announcements subsided. This is not necessarily a bad thing.

One last thing we are mindful of is stock valuations. In some respects, large-cap U.S. stocks are trading at historically high price-to-earnings (P/E) ratios, as evidenced by the chart.

Final Thoughts:

Being in the business for the past 30 years, I’ve seen my share of bull and bear markets. What I tend to see during a bull market is ordinary investors becoming overnight geniuses. They see their portfolio grow, their confidence rises with it, and the line between luck and skill suddenly becomes blurry. People stop asking why things rise, and only ask how much further they will go.

So I like to be the devil’s advocate and encourage people to stay disciplined. Things will undoubtedly shift – and when the shift occurs, it is not announced. There are no flashing lights. It sometimes begins quietly, with data that most geniuses overlook.

We’ll continue to sift through the data and be well-positioned for the ebbs and flows. Asset allocation, diversification, and rebalancing are things we continue to focus on. Markets will continue to reward disciplined investors, not just those looking to make short-term predictions. Endurance is key – it’s a marathon, not a sprint.

Brandon

US stocks surged to record highs in Q3. Markets were buoyed by strong AI-related investments, resilient corporate earnings, and expectations of future Fed rate cuts. International markets were strong as well.

While the bullish sentiment and optimism linger heading into Q4, let’s review how the various asset classes look so far this year compared to prior years (YTD through 9-30-2025):

Source: Bloomberg, FactSet, MSCI, NAREIT, Russell, Standard & Poor’s, J.P. Morgan Asset Management. Large Cap: S&P 500, Small Cap: Russell 2000, EM Equity: MSCI EME, DM Equity: MSCI EAFE, Comdty: Bloomberg Commodity Index, High Yield: Bloomberg Global HY Index, Fixed Income: Bloomberg U.S. Aggregate, REITs: NAREIT Equity REIT Index, Cash: Bloomberg 1-3m Treasury. The “Asset Allocation” portfolio is for illustrative purposes only and assumes annual rebalancing with the following weights: 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Bloomberg U.S. Aggregate, 5% in the Bloomberg 1-3m Treasury, 5% in the Bloomberg Global High Yield Index, 5% in the Bloomberg Commodity Index, and 5% in the NAREIT Equity REIT Index. Annualized (Ann.) return and volatility (Vol.) represents the period from 12/31/2009 to 12/31/2024. Please see the disclosure page at the end for index definitions. All data represent total return for stated period. Past performance is not indicative of future returns.

Looking back, here are some observations:

The third quarter of 2025 saw broad market gains, led by small-caps (@8%). Large-caps (@6%) and emerging markets (@10%) also did particularly well.The S&P 500 specifically followed up a strong second quarter with a third quarter that saw the index hit 23 record highs. Ten of the 11 sectors were positive, led by communications and technology names for the second consecutive quarter. The laggards were defensive stocks (the lone negative sector). Healthcare stocks finally turned positive for the year. Also of note, tech stocks now account for more than 50% of the US stock market cap, and defense stocks are at an all-time low (@16%)!

Here’s how the U.S. style box looked for the quarter. Notably, large-cap growth stocks and large-cap value stocks performed similarly but were both outperformed by small-cap stocks:

International markets ticked higher, with emerging markets (China, Canada) outpacing the more developed international markets (Japan, Europe). Investors diversifying their equity exposure internationally continue to be rewarded nicely in 2025 as it outperforms the U.S. by double digits.

Yields on the 10-year Treasury note ended at 4.16% for the quarter, down slightly from July. The drop in yields helped bond investors pick up some price appreciation in their portfolios. Most bond groups were up 2-3% for the previous 3 months.

Gold had another quarter of double-digit gains. Now up 46% YTD (!), the precious metal continues to benefit from geopolitical tensions, a weaker US dollar, and strong inflows from investors seeking a safe haven. The headscratcher, though, is that gold is the usual go-to when traders suspect trouble. We don’t usually see it do so well when the stock market is also doing well.

There were not many negatively performing asset classes in Q3, but oil prices slumped more than 4% in the quarter, as did copper.

Additional Discussion Points:

We just witnessed the Federal Reserve cut interest rates by 1/4 of a percentage point in September. Could we see some more cuts in the near future? Very likely. If the Fed sees proof that the economy is slowing further (due to tariffs, the job market, etc.) they’d be inclined to lower rates further. I am not into predicting rate cuts, but based on what strategists say, most anticipate another rate cut by year-end.Risks of recession have eased, but remain non-zero. We never know when we are actually IN a recession since, by definition, it’s always determined by what’s happened in the past. But we continue to hear rumblings of that coming to the surface.

What we do measure in real time is volatility. Volatility in the U.S. and international markets declined significantly in the third quarter as the shock of tariff-related announcements subsided. This is not necessarily a bad thing.

One last thing we are mindful of is stock valuations. In some respects, large-cap U.S. stocks are trading at historically high price-to-earnings (P/E) ratios, as evidenced by the chart.

Source: JP Morgan Guide to the Markets – U.S. Data are as of September 30, 2025.

This does not necessarily mean that high valuations are bad, nor that all stocks are highly valued. In fact, many of the smaller U.S. companies are considered undervalued by using the same metric. However, we do tend to see some of the largest and tech-related companies at higher valuations, and this is something we continue to monitor.Final Thoughts:

Being in the business for the past 30 years, I’ve seen my share of bull and bear markets. What I tend to see during a bull market is ordinary investors becoming overnight geniuses. They see their portfolio grow, their confidence rises with it, and the line between luck and skill suddenly becomes blurry. People stop asking why things rise, and only ask how much further they will go.So I like to be the devil’s advocate and encourage people to stay disciplined. Things will undoubtedly shift – and when the shift occurs, it is not announced. There are no flashing lights. It sometimes begins quietly, with data that most geniuses overlook.

We’ll continue to sift through the data and be well-positioned for the ebbs and flows. Asset allocation, diversification, and rebalancing are things we continue to focus on. Markets will continue to reward disciplined investors, not just those looking to make short-term predictions. Endurance is key – it’s a marathon, not a sprint.

Brandon