Q4 – 2025: Brandon’s Quarterly Market Commentary

01/09/2026Blog Categories

The end of 2025 has just passed. All major asset classes ended the year at (or near) all-time highs. It was truly another comeback story because the tariff-related market volatility earlier in the year made things feel grim. Instead, we saw a very impressive turnaround over the final 8 months of the year.

US stocks surged to record highs, and international markets well outperformed that. Bonds even had a good year. Pundits often point to the settling of the tariff negotiations and passage of the One Big Beautiful Bill Act as catalysts. Whatever the reason, disciplined and well-balanced investors continued to see their portfolios grow. And for the third year in a row.

While we do see some meaningful tailwinds heading into 2026, the situation is less than perfect. We see reasons to believe more gains will come; yet understand that factors like inflation and an unconventional administration will always introduce some unpredictability. Anything can happen – I won’t try to prognosticate. But for now, let’s review how the various asset classes did this year compared to prior years (YTD through 12-31-2025):

It was a bumpy ride to end the year, but in Q4, the S&P 500 was led by healthcare, communications, and technology names. The laggards were the utilities and real estate sectors. All sectors of the Index closed higher for the year, with the exception of real estate, which was fractionally lower.

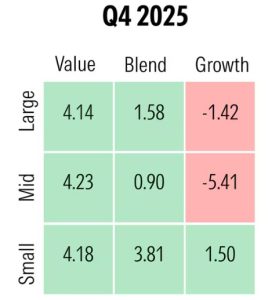

Here’s how the U.S. style box looked for the quarter. It’s obvious from the colors, but value stocks did much better in Q4 than their growth counterparts:

Overseas markets were even more rewarding than the home market, a departure from the previous couple of years. Some of the more developed countries outperformed, including Japan, Europe, and Asia. But even better were the “emerging markets”. Countries such as Korea, Chile, and South Africa led the way there. International returns in 2025 basically doubled the U.S. returns, and still offer attractive valuations as we head into 2026.

The Fed cut interest rates twice in the quarter after cutting once in the prior quarter. Yields on the 10-year Treasury note ended at 4.18% for the quarter, slightly higher from the beginning of October. Bonds had solid returns in 2025 overall, their best year since 2020.

Gold prices continued to soar to one record after another (ended the year at $4,314), and copper and silver prices also gained headline news for their surges. Crude oil prices ended the year @ $57 per barrel, down from @ $71 to start the year. Now that I am typing that, I have heard a lot about prices of things going up this past year – but not many complaining about the cost of filling up gas tanks!

Through it all, the gains in most sectors have been supported by solid economic growth and strong corporate earnings. Some would say that the bar has been raised, leaving less room for positive surprises.

Without doubt, the memories of the global financial crisis and the Covid pandemic are still somewhat fresh in our minds. That may lead us to think that 3 consecutive years of double-digit stock market returns should prompt us to lock in gains. No one knows how 2026 will perform, but I’d encourage everyone to focus on the road ahead. Multi-year runs of positive returns are not uncommon. As legendary investor Peter Lynch said,

Consider how we started 2025, coming fresh out of two 20%+ years in the markets. Were many thinking we’d get another double-digit year? Not many, from what I saw. Despite major policy and macro disruptions, the markets and global economy showed remarkable resilience. Again, we cannot predict the future, but I like to keep things in perspective.

2025 will be known as a year driven by policy shifts (a new administration, trade developments, tax bill, etc.). The focus shifts in 2026 to how the economy responds to those policies. We’ve got a healthy consumer, stimulus from the tax bill, and continued AI spending. But we are also keeping an eye on the labor market weakness and the effect the tariffs will have. We’ll continue to do our part, looking for evolving trends.

I have learned in my years in the business that it is best to avoid short-term market prognostications. In the short run, it’s a pure guess. But in the long run, it’s math.

Equally important is avoiding the temptation to believe the good times are here to stay. The price of admission for successful long-term investing is inevitable periods of market swings and volatility. Yes, we’ve had three strong years in a row. But sound investing celebrates doing the right thing, regardless of prevailing market conditions.

Best wishes in 2026!

Brandon

US stocks surged to record highs, and international markets well outperformed that. Bonds even had a good year. Pundits often point to the settling of the tariff negotiations and passage of the One Big Beautiful Bill Act as catalysts. Whatever the reason, disciplined and well-balanced investors continued to see their portfolios grow. And for the third year in a row.

While we do see some meaningful tailwinds heading into 2026, the situation is less than perfect. We see reasons to believe more gains will come; yet understand that factors like inflation and an unconventional administration will always introduce some unpredictability. Anything can happen – I won’t try to prognosticate. But for now, let’s review how the various asset classes did this year compared to prior years (YTD through 12-31-2025):

Source: Bloomberg, FactSet, MSCI, NAREIT, Russell, Standard & Poor’s, J.P. Morgan Asset Management. Large Cap: S&P 500, Small Cap: Russell 2000, EM Equity: MSCI EME, DM Equity: MSCI EAFE, Comdty: Bloomberg Commodity Index, High Yield: Bloomberg Global HY Index, Fixed Income: Bloomberg U.S. Aggregate, REITs: NAREIT Equity REIT Index, Cash: Bloomberg 1-3m Treasury. The “Asset Allocation” portfolio is for illustrative purposes only and assumes annual rebalancing with the following weights: 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Bloomberg U.S. Aggregate, 5% in the Bloomberg 1-3m Treasury, 5% in the Bloomberg Global High Yield Index, 5% in the Bloomberg Commodity Index, and 5% in the NAREIT Equity REIT Index. Annualized (Ann.) return and volatility (Vol.) represents the period from 12/31/2009 to 12/31/2025. Please see the disclosure page at the end for index definitions. All data represent total return for stated period. Past performance is not indicative of future returns.

Looking back, here are some observations:

Since most people look at the S&P 500 Index, we’ll start there first. After surging 26.3% in 2023 and 25% in 2024, the Index followed up with a total return of 17.9% in 2025. This capped 3 consecutive years of exceptional performance.It was a bumpy ride to end the year, but in Q4, the S&P 500 was led by healthcare, communications, and technology names. The laggards were the utilities and real estate sectors. All sectors of the Index closed higher for the year, with the exception of real estate, which was fractionally lower.

Here’s how the U.S. style box looked for the quarter. It’s obvious from the colors, but value stocks did much better in Q4 than their growth counterparts:

Overseas markets were even more rewarding than the home market, a departure from the previous couple of years. Some of the more developed countries outperformed, including Japan, Europe, and Asia. But even better were the “emerging markets”. Countries such as Korea, Chile, and South Africa led the way there. International returns in 2025 basically doubled the U.S. returns, and still offer attractive valuations as we head into 2026.

The Fed cut interest rates twice in the quarter after cutting once in the prior quarter. Yields on the 10-year Treasury note ended at 4.18% for the quarter, slightly higher from the beginning of October. Bonds had solid returns in 2025 overall, their best year since 2020.

Gold prices continued to soar to one record after another (ended the year at $4,314), and copper and silver prices also gained headline news for their surges. Crude oil prices ended the year @ $57 per barrel, down from @ $71 to start the year. Now that I am typing that, I have heard a lot about prices of things going up this past year – but not many complaining about the cost of filling up gas tanks!

Through it all, the gains in most sectors have been supported by solid economic growth and strong corporate earnings. Some would say that the bar has been raised, leaving less room for positive surprises.

Additional Discussion Points:

As our small print disclaimers emphasize, past performance is no guarantee of future results. But neither should past performance make us nervous, either. We always want to keep the big picture in mind.Without doubt, the memories of the global financial crisis and the Covid pandemic are still somewhat fresh in our minds. That may lead us to think that 3 consecutive years of double-digit stock market returns should prompt us to lock in gains. No one knows how 2026 will perform, but I’d encourage everyone to focus on the road ahead. Multi-year runs of positive returns are not uncommon. As legendary investor Peter Lynch said,

Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.

Consider how we started 2025, coming fresh out of two 20%+ years in the markets. Were many thinking we’d get another double-digit year? Not many, from what I saw. Despite major policy and macro disruptions, the markets and global economy showed remarkable resilience. Again, we cannot predict the future, but I like to keep things in perspective.

Final Thoughts:

2025 will be known as a year driven by policy shifts (a new administration, trade developments, tax bill, etc.). The focus shifts in 2026 to how the economy responds to those policies. We’ve got a healthy consumer, stimulus from the tax bill, and continued AI spending. But we are also keeping an eye on the labor market weakness and the effect the tariffs will have. We’ll continue to do our part, looking for evolving trends.

I have learned in my years in the business that it is best to avoid short-term market prognostications. In the short run, it’s a pure guess. But in the long run, it’s math.

Equally important is avoiding the temptation to believe the good times are here to stay. The price of admission for successful long-term investing is inevitable periods of market swings and volatility. Yes, we’ve had three strong years in a row. But sound investing celebrates doing the right thing, regardless of prevailing market conditions.

Best wishes in 2026!

Brandon